In these difficult times for the tourism industry in general and for the car rental industry, WeYield has decided to aggregate anonymized data from the various clients we have per geographical zone. The goal is to share some key performance indicators for the months of April and July 2020 from our WeYield apps and compare the situation of them between two reference dates (1st and 15th of March 2020).

These data have no statistic mean due to limited set of companies but more to step back and enlarge the perspective to other area on the planet.

Take care.

APRIL 2020 :

- Fleet has been reduced a bit vs last year at -4%. However, no significant change in past two weeks.

- Utilization is declining at -9ps vs last year and Easter-Spring breaks will see a major fall in volume (-27% in on-rent days vs last year). It has continued to go down over the last two weeks by -1 pt while it had picked-up by +36pts over the same two-week res period of last year.

- RPD is moving up impressively, +26% vs last year and it has continued to go further up over the last two weeks by +42% (while increase was cooler during the same interval last year).

- Conclusion: demand will not come due to the lock-down. But countries have compensated volume drops by having higher RPD this year.

JULY 2020 :

- Fleet has been reduced a bit vs last year by -2%. The trend between 1st and 15th March 2020 is flat (as it was during the same interval of dates last year).

- Demand is in advance significantly +15% and trend is positive from 1st to 15th March of reservation but not enough compared to the +28% of last year pick-up.

- Utilization is still small but under a slight acceleration vs last year and has continued to pick-up slowy over the last two weeks.

- RPD is down 18% versus last year and down 23% versus two weeks ago, suggesting many operators are lowering their prices.

- Conclusion: situation may change due to recent lockdown decided by many Governements of these countries (New Zealand, Thailand)

APRIL 2020 :

- Fleet is down by 6% vs last year with no observed changed in past two weeks.

- Utilization is down 12pts vs last year. Easter-Spring breaks will see a fall in volume (-18% in on-rent days vs last year) and last two weeks has shown a 9% increase.

- RPD is down by -16% vs last year but we can note that it is only slighty going down by -1% in past two weeks (while it was down 2% during the same interval last year).

- Conclusion: demand will not come due to the new lock-down that has just started. Keep the prices up to avoid any revenue spoilage that will not generate any new demand.

JULY 2020 :

- Fleet for July is decreasing by -2% vs last year with no observed changes in past two weeks.

- Demand is down significantly by 14% vs last year, but we have seen a 15% increase in past two weeks, the same as we observed last year.

- Utilization is still small at 17% down 3 points vs last year with only a minor +3 points increase in past two weeks (3 points gain in same interval last year).

- RPD however down by 14% vs last year (with -2% in past two weeks,vs -1% previous year).

- Conclusion: keep calm and maintain current price levels. When the virus is defeated, we anticipate a major reservation flow. Be ready at a good price.

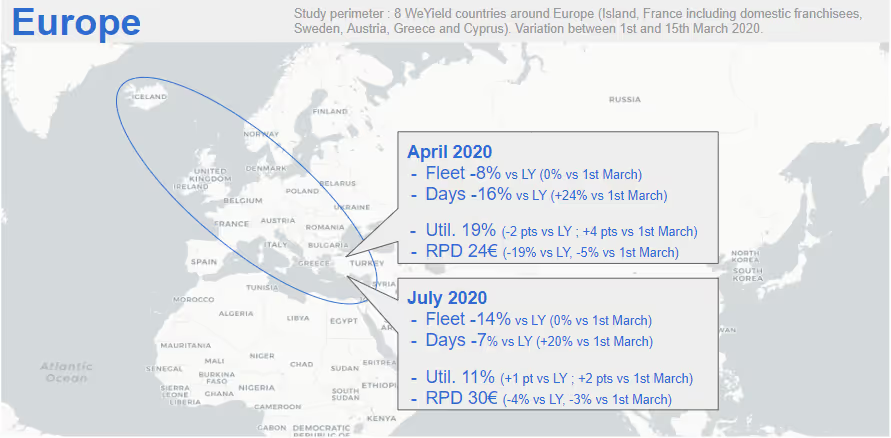

APRIL 2020 :

- Fleet has been reduced a bit vs last year at -8%. However, no fleet changes observed in last two weeks.

- Utilization is down by 2pts vs last year and Easter-Spring breaks will see a major fall in volume (-16% in on-rent days vs last year). However we gained 24% in past two weeks yet this is half the gain of the same 2 week period last year.

- RPD has dropped by 19% vs last year and by a further 5% in past two weeks, versus a minor gain in RPD in same period last year.

- Conclusion: Demand is weak but further price drops are not necessary. When the virus will be defeated, we anticipate a major reservation flow. Be ready at a good price.

JULY 2020 :

- Utilization is still small at 11% but 1pt up versus last year and growing at same rate as last year over the previous 2 weeks.

- Fleet has been reduced vs last year by -14%. No observed fleet changes in past two weeks.

- Demand is down by -7% versus last year, however has picked up by 205 in past two weeks, similar to the previous year.

- RPD is down slight versus last year at -4% and dropped by 3% in past two weeks.

- Conclusion: keep calm and maintain current price levels. When the virus is defeated, we anticipate a major reservation flow. Be ready at a good price.

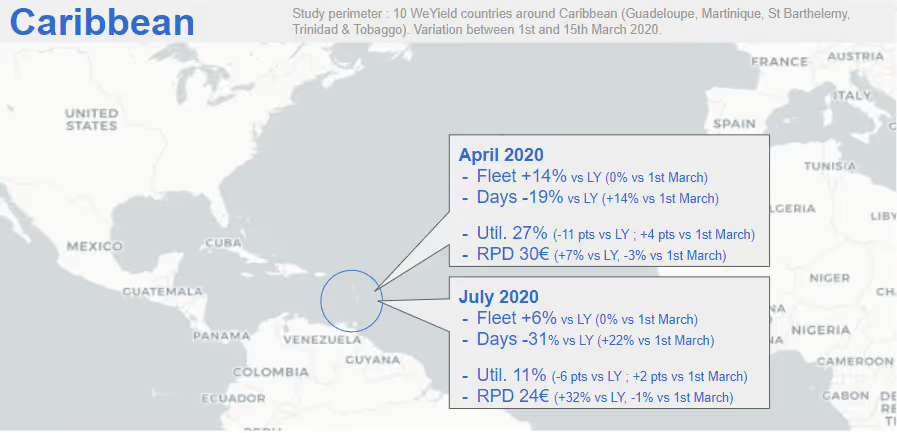

APRIL 2020 :

- Fleet has increased vs last year at +15% (no change in last two weeks).

- Utilization is down by 11pts vs last year and Easter-Spring breaks will see a major fall in volume (-19% in on-rent days vs last year) even though it is improving over the last two weeks with +14% while it was pick-up +23% over the same two-week res period of last year.

- RPD is up by 7% vs last year but has decreased by -3% in last two weeks.

- Conclusion: demand will not come due to the new lockdown that has just started. Keep the prices up to avoid any revenue spoilage that will not generate any new demand.

JULY 2020 :

- Fleet is up by 6% versus last year for July, with no changes in past two weeks.

- Utilization is still small at 11% and down by 6 pts versus last year, the last two weeks has seen slower util growth than same time last year.

- Demand is down -31% versus last year but trends is positive (+22%) from 1st to 15th March of reservation but not enough compared to the +50% of last year pick-up.

- RPD is at a good level at 24€ with a nice +32% vs last year proving the calm of operators for upcoming high season. However, we can note already a slight but moderate reduction of RPD by -1% in past two weeks (but it was -18% last year during the same interval).

- Conclusion: keep calm and maintain current price levels. When the virus is defeated, we anticipate a major reservation flow. Be ready at a good price.

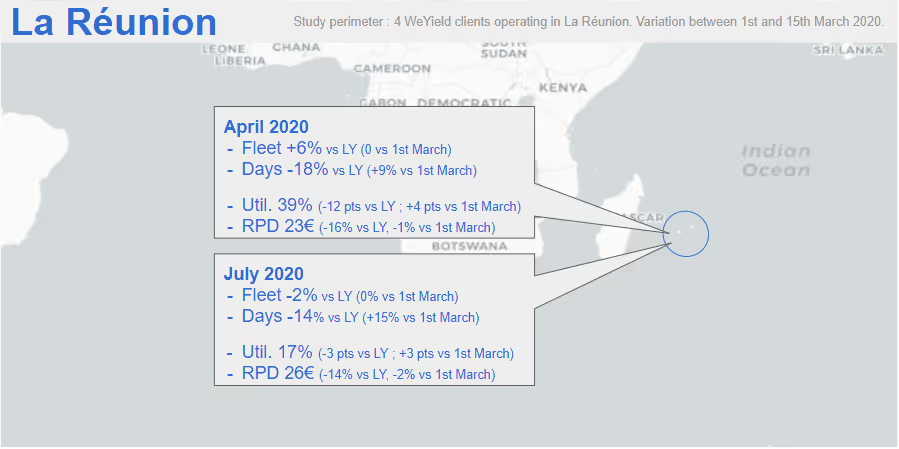

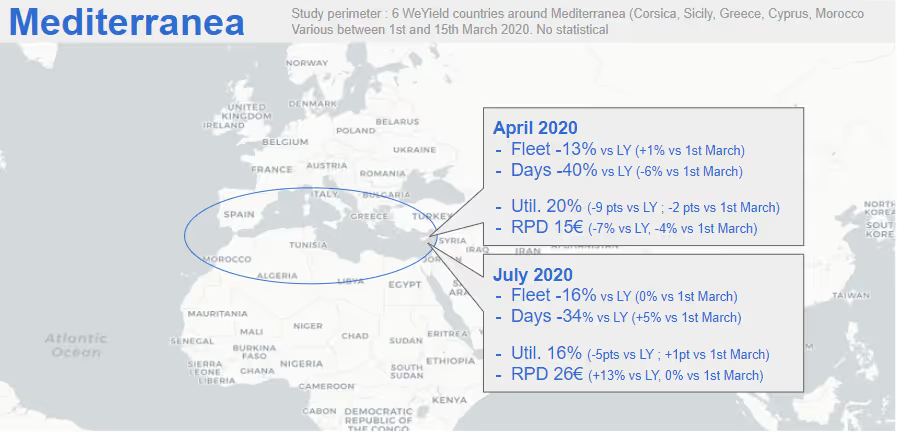

APRIL 2020 :

- Utilization is stabilizing at 20%, down 9pts vs last year. Easter-Spring breaks will be a major fall in volume (-40% in on-rent days vs last year) and last two weeks has not shown any major increase.

- Fleet has decreased vs last year by -13% (1% change in two weeks, last year saw a significant decrease in fleet).

- RPD is down by -7% vs last year but we can note that it is slighty going down by -4% in past two weeks (while it was up 11% during the same interval last year).

- Conclusion: demand will not come due to the new lock-down that has just started. Keep the prices up to avoid any revenue spoilage that will not generate any new demand

JULY 2020 :

- Utilization is still small at 16% down 5pts vs last year with only a minor +1pt increase in past two weeks (3pts gain in same interval last year).

- Fleet for July is decreasing by -16% with no observed changes in past two weeks.

- Demand is down significantly by 34% vs last year, with only a 5% increase in past two weeks vs +16% in same time interval last year.

- RPD however up by 13% vs last year although did not change in past two weeks (last year same interval saw 2% increase.

- Conclusion: keep calm and maintain price levels. When the virus is defeated, we anticipate a major reservation flow. Be ready at a good price

APRIL 2020 :

- Utilization has increased a lot by +18pts vs last year and Easter-Spring breaks were showing some demand (but corporate monthly rental artificially sustain the volume), particularly in last two weeks when compared to last year.

- Fleet has been reduced a bit vs last year at -7% with no change in fleet in last two weeks.

- RPD is unfortunately down by 48% versus last year explaining the higher utilisation, and has reduced by 14% in last two weeks.

- Conclusion: Demand is still present, further price drops are not necessary. When the virus is defeated, we anticipate a major reservation flow. Be ready at a good price

JULY 2020 :

- Fleet has been reduced significantly vs last year by -15%. No observed fleet changes in past two weeks.

- Utilization is up by 10pts versus last year and significantly increased by 9pts in past two weeks.

- Demand is in advance significantly +109% with strong growth in last two weeks versus same period last year.

- RPD is however decreasing at -19% vs last year and down by 12% in last two weeks, comparatively we saw a small 5% increase in same period last year.

- Conclusion: keep calm and do not panic drop your prices as demand still exists. When the virus is defeated, we anticipate a major reservation flow. Be ready at a good price.